Last Update: June 20, 2022

ARIMA Models Identification: Correlograms are used to identify ARIMA models autoregressive and moving average orders.

As example, we can delimit univariate time series into training range

for model fitting and testing range

for model forecasting.

Then, we can do training range univariate time series model autoregressive

and moving average

orders identification by estimating sample autocorrelation and partial autocorrelation functions correlograms. Notice that we need to evaluate whether level or

order differentiated training range univariate time series is needed for ARIMA model integration

order.

Next, we estimate training range univariate time series sample autocorrelation function correlogram with formula . Training range univariate time series estimated lag

sample autocorrelation function

is the estimated sample covariance between univariate time series

and its lag

univariate time series

divided by univariate time series estimated sample variance

. Training range autocorrelation function is the linear dependence between current

and lagged

univariate time series data.

After that, we estimate training range sample autocorrelation function correlogram confidence intervals with formula . Training range sample autocorrelation function confidence intervals

are the inverse of the standard normal cumulative distribution

with probability equal to one minus statistical significance level

divided by two and this result multiplied by the square root of one plus two times the sum of sample autocorrelation function square values

divided by number of observations

. Notice that we need to evaluate whether Bartlett formula is needed for sample autocorrelation function correlogram confidence intervals estimation.

Later, we estimate training range univariate time series sample partial autocorrelation function correlogram with formula . Training range univariate time series lag

sample partial autocorrelation function

can be estimated through lag

linear regression estimated coefficient

with formula

. Training range partial autocorrelation function is the linear dependence between current

and lagged

univariate time series data after removing any linear dependence on

. Notice that we can also estimate sample partial autocorrelation function using Yule-Walker, Levison-Durbin or adjusted linear regression methods.

Then, we estimate training range sample partial autocorrelation function correlogram confidence intervals with formula . Training range sample partial autocorrelation function confidence intervals

are the inverse of the standard normal cumulative distribution

with probability equal to one minus statistical significance level

divided by two and this result multiplied by one divided by the square root of number of observations

.

Next, we can do training range univariate time series model autoregressive

and moving average

orders identification.

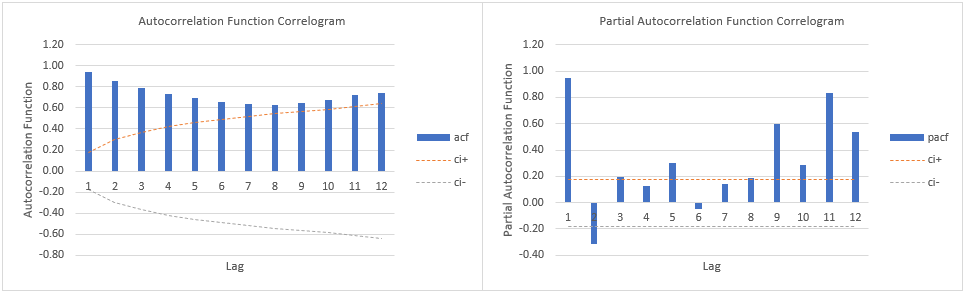

- If sample autocorrelation function correlogram

tails of gradually and sample partial autocorrelation function correlogram

drops after

statistically significant lags then we can observe the potential need of an autoregressive model

of order

- Alternatively, if sample autocorrelation function correlogram

statistically significant lags and sample partial autocorrelation function correlogram

of order

- Otherwise, if sample autocorrelation function correlogram

of orders

Below, we find example of training range univariate time series model autoregressive

and moving average

orders identification correlograms using airline passengers data [1]. Training range as first ten years and testing range as last two years of data. Correlograms confidence intervals with

statistical significance level. Notice that correlograms confidence intervals statistical significance level was only included as an educational example which can be modified according to your needs.

References

[1] Data Description: Monthly international airline passenger numbers in thousands from 1949 to 1960.

Original Source: Box, G. E. P., Jenkins, G. M. and Reinsel, G. C. (1976). “Time Series Analysis, Forecasting and Control”. Third Edition. Holden-Day. Series G.

Source: datasets R Package AirPassengers Object. R Core Team (2021). “R: A language and environment for statistical computing”. R Foundation for Statistical Computing, Vienna, Austria.